Orange County Bancorp, Inc. Announces Record First Quarter 2021 Results

FOR IMMEDIATE RELEASE

Orange County Bancorp, Inc. Announces Record First Quarter 2021 Results

- Net Income for Q1 2021 increased by $2.5 million, or 103%, to a record $5.03 million compared to Q1 2020

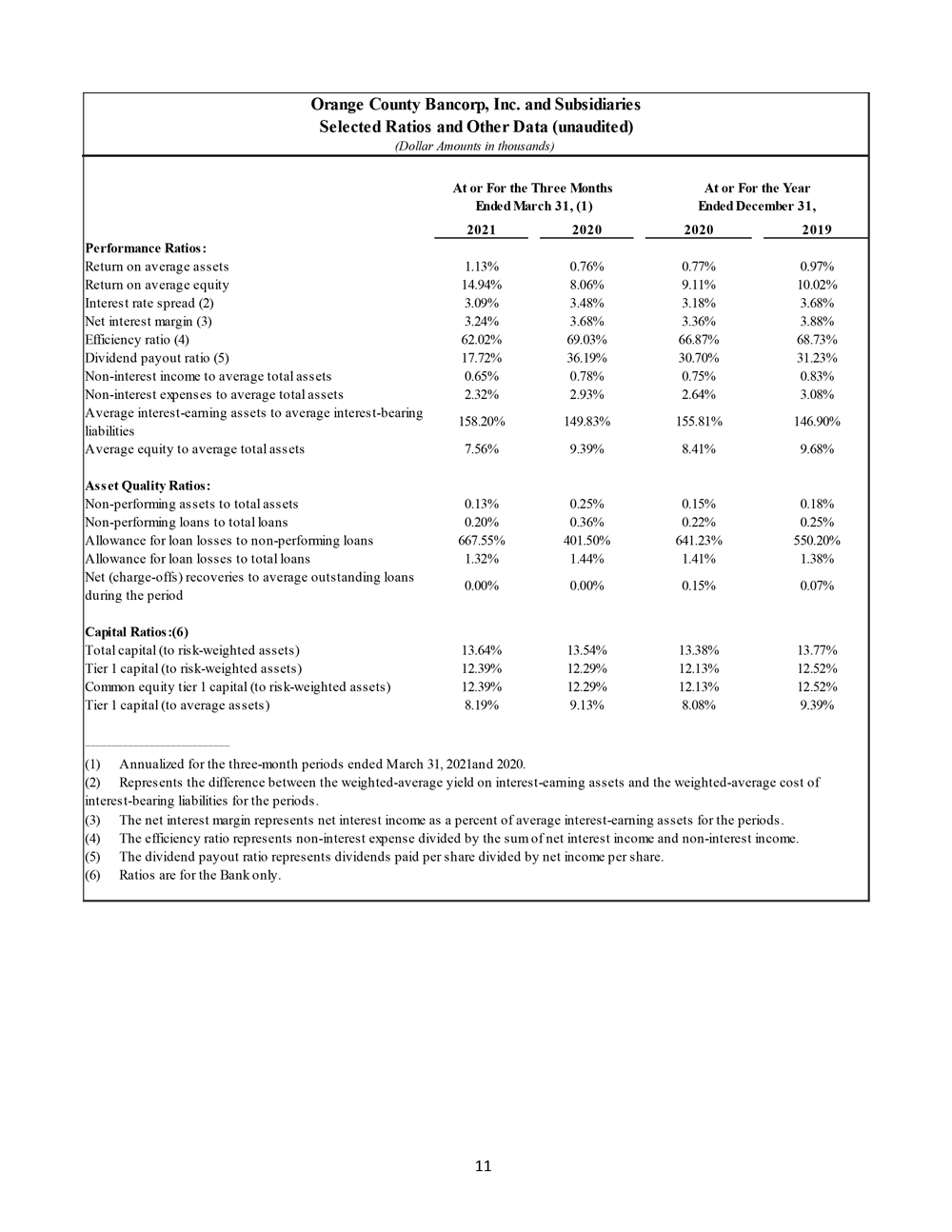

- Return on average assets for Q1 2021 rose 37 basis points year-over-year to 1.1%

- Return on common equity for Q1 2021 rose 688 basis points year-over-year to 14.9%

- Loan loss provision for Q1 2021 of $66 thousand was $1.1 million below the same period last year due to stabilizing credit trends

- Average Loans (net of PPP) for Q1 2021 increased 18.5% year-over-year, to $1.1 billion

- Average Demand Deposits grew 60.1% year-over-year to $552.4 million

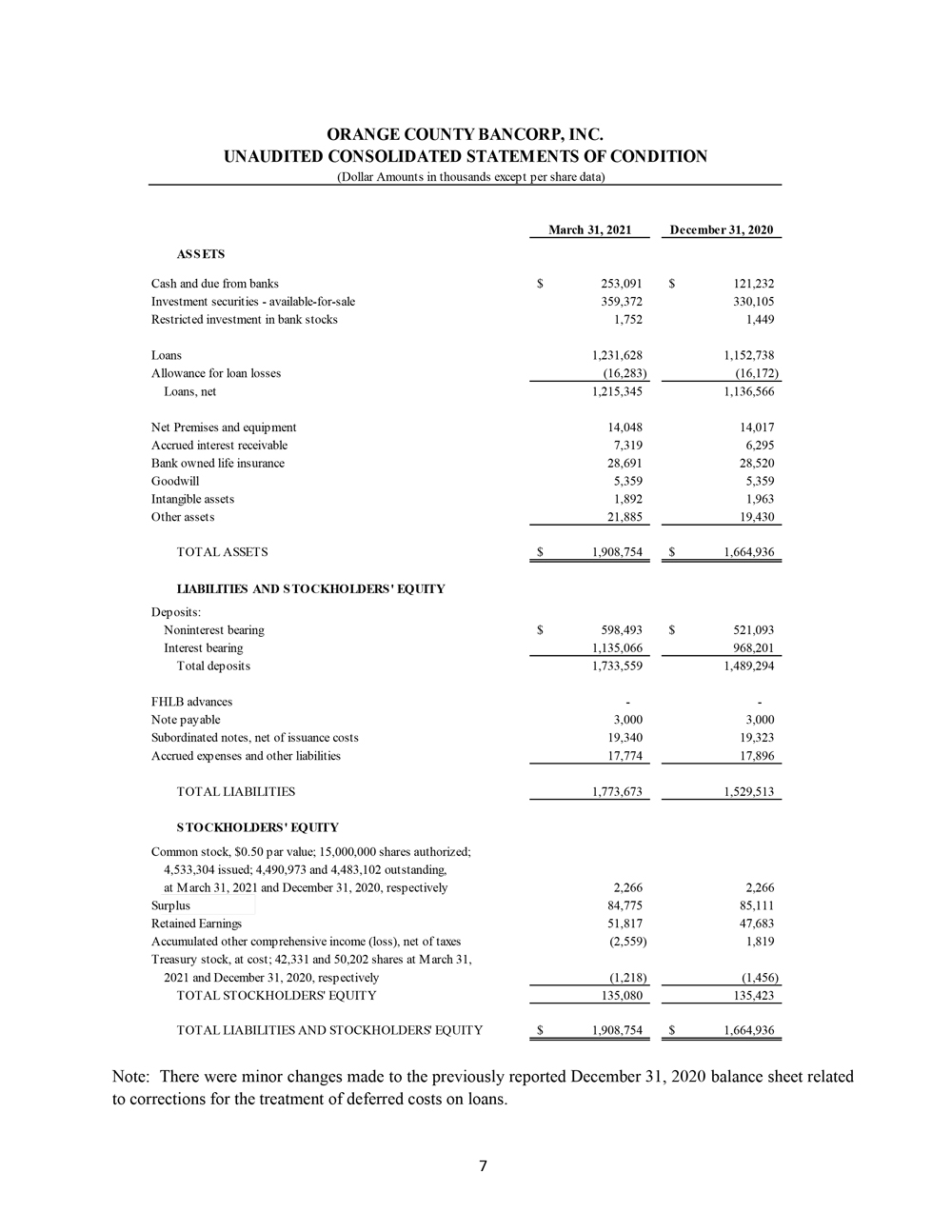

- Total Assets grew $243.8 million, or 14.6% from year-end 2020 to $1.9 billion

- Trust and asset advisory business revenue increased 18.6% to $2.3 million for the quarter

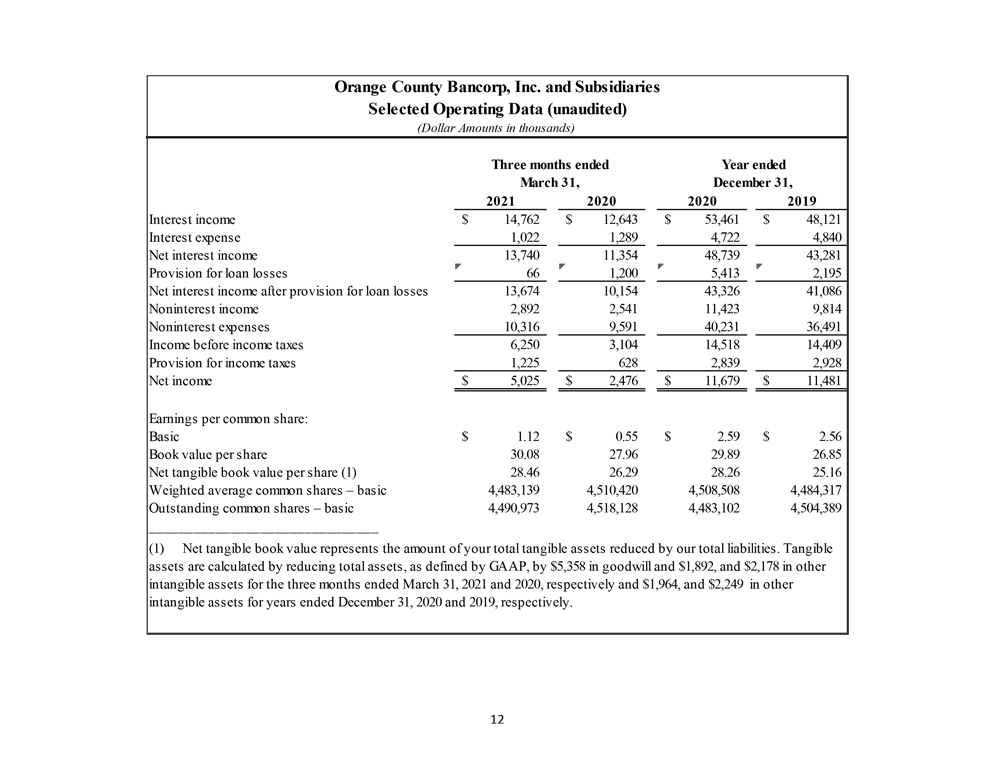

MIDDLETOWN, N.Y., MAY 3, 2021 – Orange County Bancorp, Inc. (the “Company” – OTCQX: OCBI), parent of Orange Bank & Trust Co. (the “Bank”) and Hudson Valley Investment Advisors, Inc. (HVIA), today announced net income of $5.03 million, or $1.12 per share, for the three months ended March 31, 2021. This compares with net income of $2.48 million, or $0.55 per share, for the three months ended March 31, 2020.

“I am extremely proud of the results our team produced this quarter,” said Orange County Bancorp President & CEO, Michael Gilfeather. “They reflect the earnings power of our focused and deliberate strategy to grow the Bank and make it a more accessible and important partner for our clients in Orange, Rockland and Westchester Counties. The momentum we were building in 2020, despite the considerable challenges presented by COVID, carried into the first quarter of 2021, resulting in 105% year-over-year growth in net income to a record of over $5 million.

Our core lending business has been and remains strong, with loan growth, net of PPP, up over 18.5% in the first quarter of 2021 versus the same period last year. Many of the compelling opportunities reflected in these figures emerged late last year and continued into the recent quarter. While new loan demand is weighted toward commercial real estate, for which the Bank remains well within conservative concentration limits, overall loan activity remains diverse across both industries and the region we serve. Additionally, despite meaningful growth in the size of our loan portfolio, improving economic and credit trends allowed us to reduce our provision for loan losses more than $1 million versus the same quarter last year. Loans on deferral also continued to decline, finishing the first quarter at just over $32 million, or 2.6% of our loan portfolio, down from nearly 30% at the end of our June quarter in 2020.

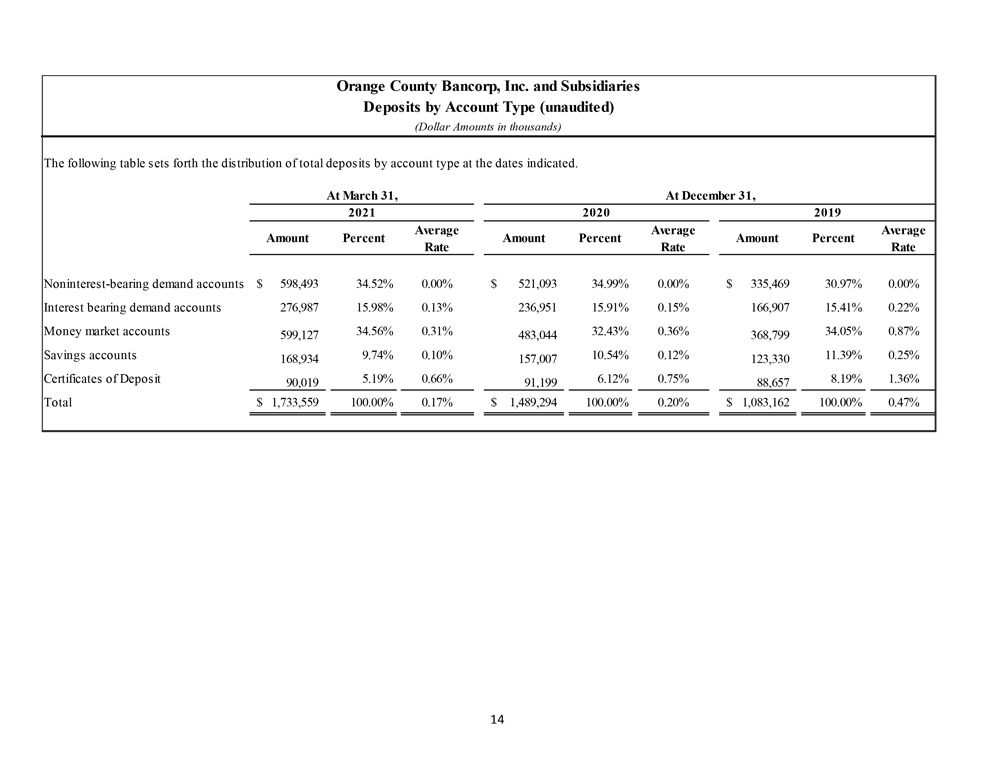

As has been widely reported, the Federal Reserve responded to the financial shock of the pandemic last Spring by slashing interest rates and injecting unprecedented liquidity into the banking system. This helped stabilize the economy, but now has the banking system confronting the challenge of elevated deposit levels and narrower lending margins. We sought to manage this by attracting a greater share of business clients’ non-interest bearing deposits. The results surpassed expectations, with Average Demand Deposits increasing more than 60% during the quarter versus the same period last year, while total deposits grew to over $1.7 billion. This effort blunted margin pressure during the quarter and should continue to reduce the deposit volatility that often accompanies Fed action in response to changing economic trends.

Another significant development the Bank actively engaged in during the COVID-19 pandemic was the federally-funded Paycheck Protection Program (PPP). Our early decision to participate was driven by recognition of the vital role this program could play in supporting the economic viability of our business clients. While the Bank has enjoyed some revenue from the program, primarily through monthly interest rate accruals and the “true-up” fee when PPP loans are forgiven, we view this income as unique to the time and tangential to our core business. This said, we remain actively involved with clients on the second round of PPP financing and anticipate loan volume may well approach levels we saw during its initial phase.

In addition to these activities, the Company’s newly created Orange Wealth Management initiative, which includes our private bank, trust, and HVIA advisory business, saw revenue grow nearly 19%, to $2.3 million, versus the same quarter last year. This growth stemmed primarily from a $41 million increase, to $1.2 billion, in assets under management (AUM). To further support this program, the Bank hired veteran banker Ron Coccaro, who will be responsible for identifying and pursuing new growth and sales opportunities. We expect growth and opportunities to result from broader adoption and integration of our Wealth Solutions service, which combines best-in-class technology with top rated financial advisors to give our clients an accurate, comprehensive picture of their financial health and strategies for long-term growth and security.

We are also currently building new branches in the Bronx and Nanuet, and anticipate opening the former in late June or early July, with the latter to follow shortly thereafter. We view these locations as very natural and logical extensions for the Bank, with our regional footprint and experience giving us confidence in their potential. We look forward to these openings and further expanding the Bank’s reach.

Orange Bank’s successful 127-year operating history has been characterized by cautious lending standards and thoughtful, patient growth. This legacy guides our decision making today, with any contemplated changes or additions to our service offerings evaluated in terms of their impact on our community, clients, and investors. Our record first quarter 2021 results indicate we are succeeding on all three fronts, and provide a strong foundation for the year ahead. Rest assured we will remain vigilant in our efforts and continue to build on these accomplishments.”

First Quarter 2021 Financial Review

Net Income

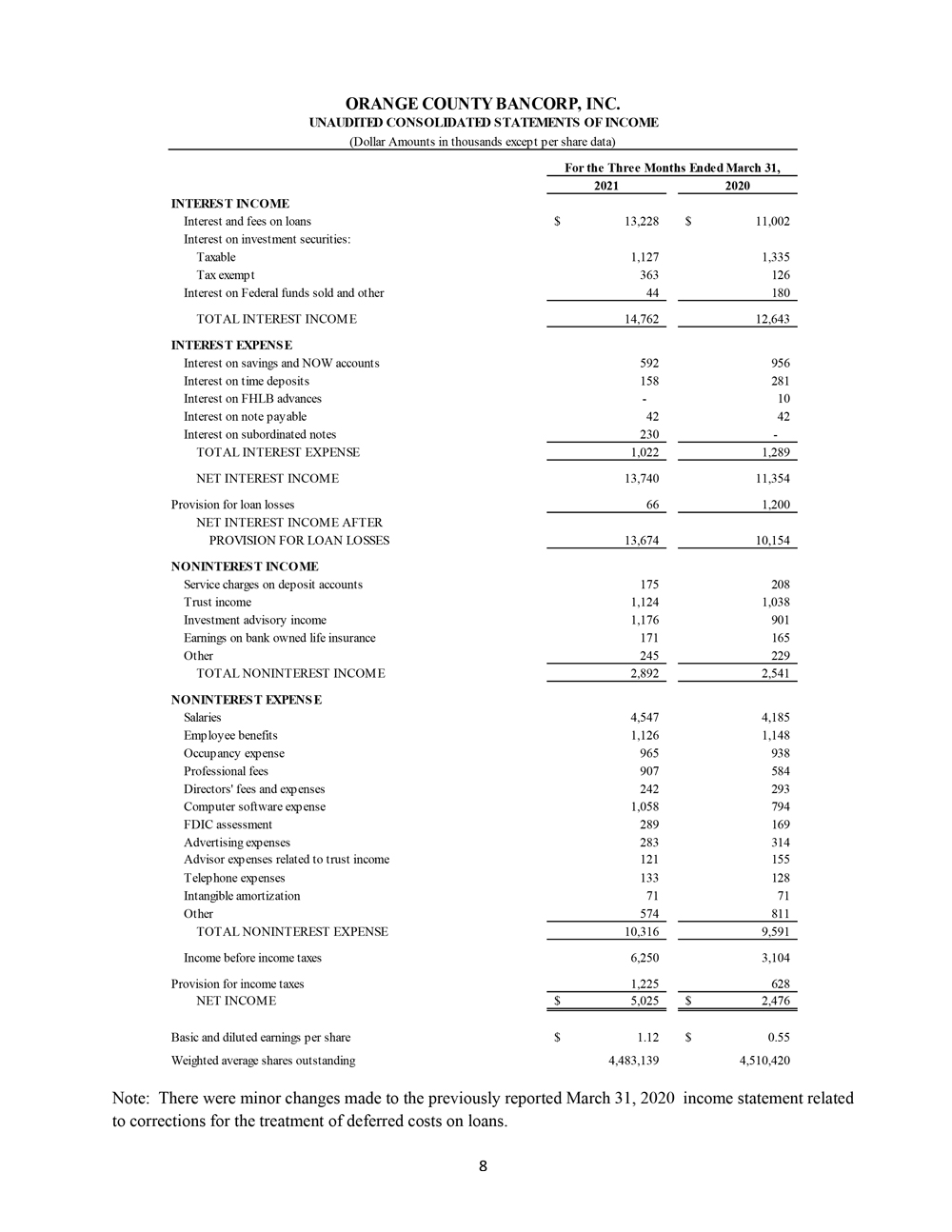

Net income for the first quarter of 2021 was $5.03 million, compared to net income of $2.48 million for the first quarter of 2020, an increase of $2.55 million, or 105%. The increase was driven primarily by growth in net interest income and a concurrent decrease in the provision for loan losses, partially offset by an increase in non-interest expense.

Net Interest Income

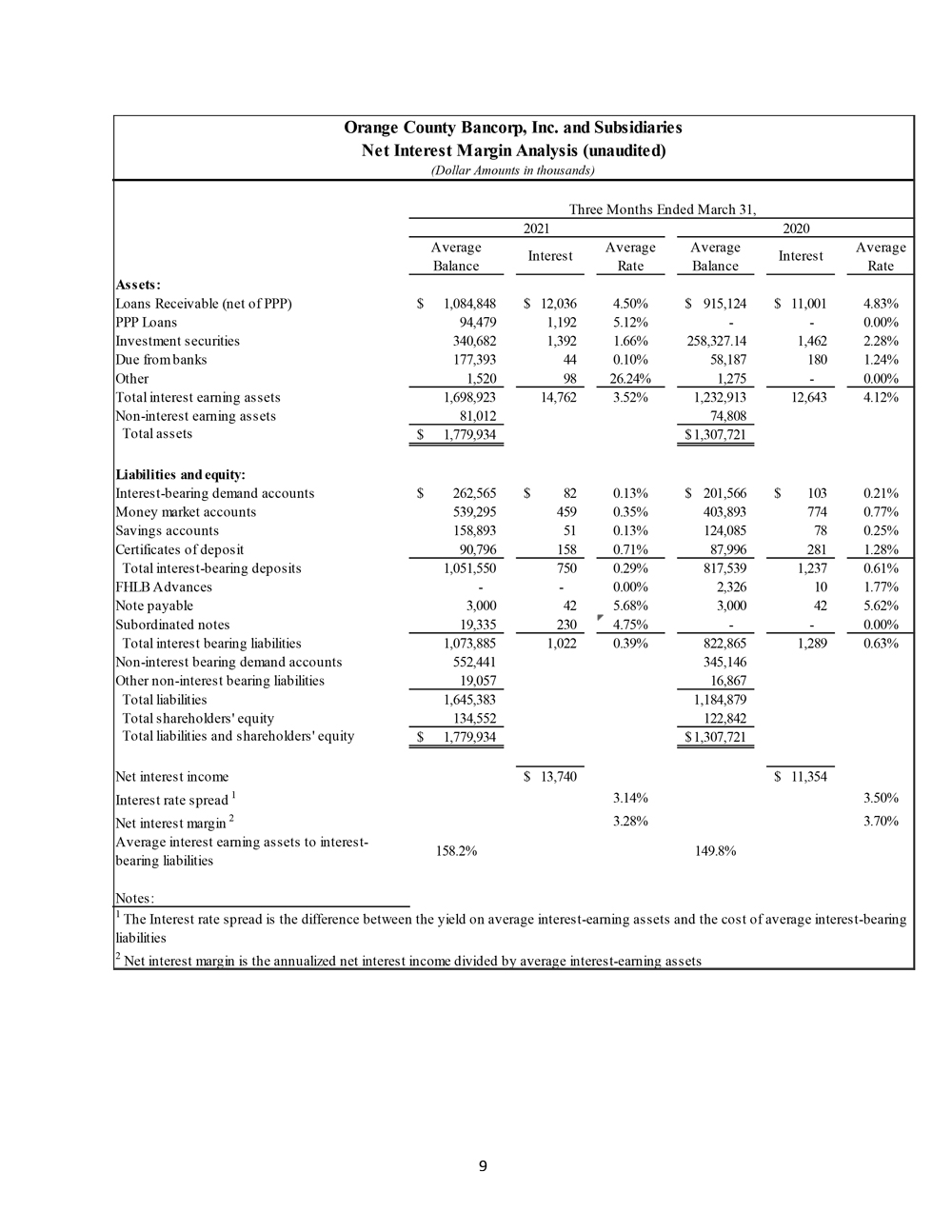

For the three months ended March 31, 2021, net interest income increased $2.4 million, or 21.0%, versus the same period last year.

Total interest income increased $2.1 million, or 16.6%, for the three months ended March 31, 2021 versus the corresponding period last year. This increase in interest income was primarily due to loan growth and fees associated with PPP loan forgiveness.

Total interest expense decreased $267 thousand in the first quarter of 2021, to $1.0 million, compared to $1.3 million in the first quarter of the prior year. The decrease resulted from a $487 thousand reduction in deposit interest expense partially offset by an increase in interest expense of $230 thousand due to the subordinated debt issued in September 2020. Lower interest expense on deposits was consistent with the reduction of the Fed Funds rate in the first quarter of 2020 in response to the COVID-19 pandemic.

Provision for Loan Losses

The Company recognized a $66 thousand provision for loan losses for the three months ended March 31, 2021, well below the $1.2 million provision for loan losses recorded in the same period in the prior year. The lower provision reflects significantly improved credit metrics and loan deferrals. The allowance for loan losses to total loans was 1.32% as of March 31, 2021. Excluding PPP loans, the ratio was 1.46% as of March 31, 2021.

Non-Interest Income

Non-interest income was $2.9 million during the first quarter of 2021, an increase of $351 thousand, or 13.8%, versus the first quarter of 2020. The increase was a result of continued growth in the Bank’s trust operations and HVIA’s asset management activities.

Non-Interest Expense

Non-interest expense was $10.3 million during the first quarter of 2021, an increase of $725 thousand, or 7.6%, versus the first quarter of 2020 due to the Bank’s continued investment in growth. Continued investment to support growth was comprised primarily of a $362,000 increase in salaries, a $264,000 increase in information technology costs and a $120,000 increase in deposit insurance expense resulting from the significant growth in deposit balances. The efficiency ratio improved 701 basis points during the first quarter of 2021, to 62.02%, compared with the same period last year.

Income Tax Expense

Income tax accrual for the three months ended March 31, 2021 was $1.2 million versus $628 thousand for the same period in 2020 due to the increase in income before income tax expense. The effective tax rates for the two periods were 19.6% and 20.2%, respectively.

Financial Condition

Total consolidated assets increased $243.8 million, or 14.6%, from $1.66 billion at December 31, 2020 to $1.91 billion at March 31, 2021. The increase in total consolidated assets reflected increases in cash and due from banks, loans receivable and investments.

Total cash and due from banks increased from $121.2 million at December 31, 2020 to $253.1 million at March 31, 2021, an increase of $131.9 million, or 108.8%. The increase in cash was primarily due to increases in deposit account balances driven by seasonal increases in municipal deposits, ongoing success attracting business account assets, and government efforts to increase liquidity in the economy.

Total investments increased $29.3 million from $330.1 million at December 31, 2020 to $359.4 million at March 31, 2021. The increase was primarily in mortgage backed and municipal securities.

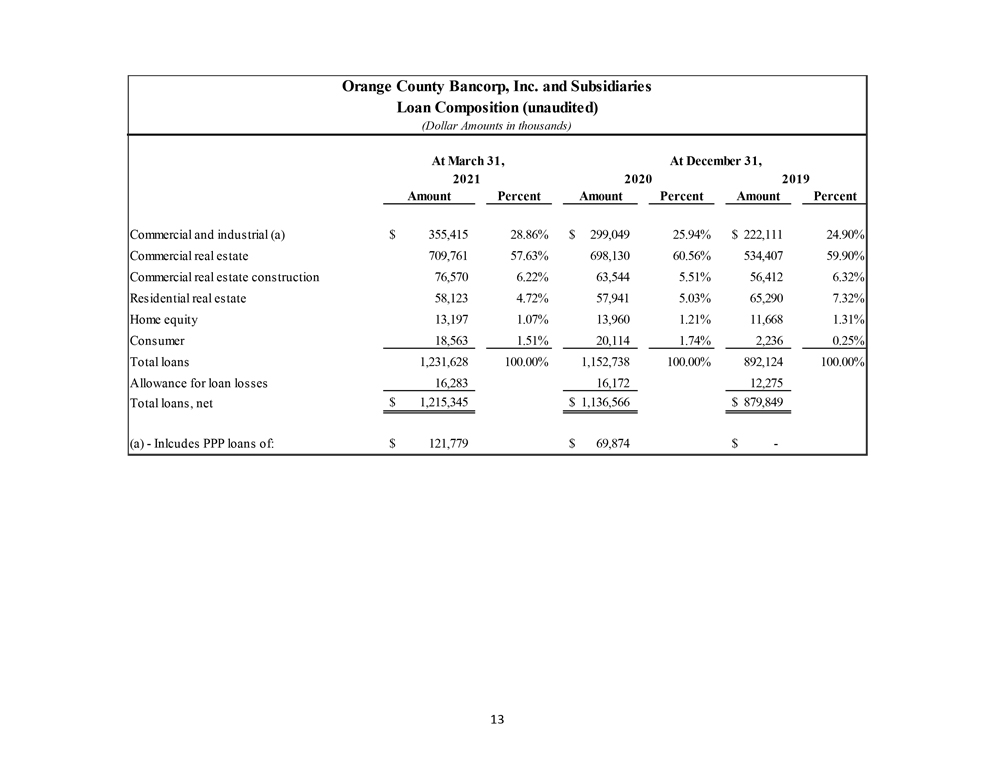

Total loans increased from $1.15 billion at December 31, 2020 to $1.23 billion at March 31, 2021, an increase of $80.0 million. This increase was due primarily to a $51.9 million increase in PPP loans.

Total deposits increased $244.3 million to $1.73 billion at March 31, 2021, from $1.49 billion at December 31, 2020. While the increase was primarily related to increases in business accounts, it included $80.6 million of seasonal inflows of government and municipal deposits attributable to the cyclical nature of real estate tax collections.

Borrowed funds of $22.3 million at March 31, 2021 was unchanged from December 31, 2020.

Stockholders’ equity remained relatively flat at $135.1 million at March 31, 2021 as the $4.1 million increase in retained earnings during the first quarter of 2021 was offset by the $4.4 million decline in AOCI, for the same period, resulting from the impact of higher interest rates on the market value of investments.

At March 31, 2021, the Bank maintained capital ratios in excess of regulatory standards for well capitalized institutions. The Bank’s Tier 1 capital to average assets ratio was 8.19%, both the common equity and Tier 1 capital to risk weighted assets were 12.39% and the total capital to risk weighted assets ratio was 13.64%.

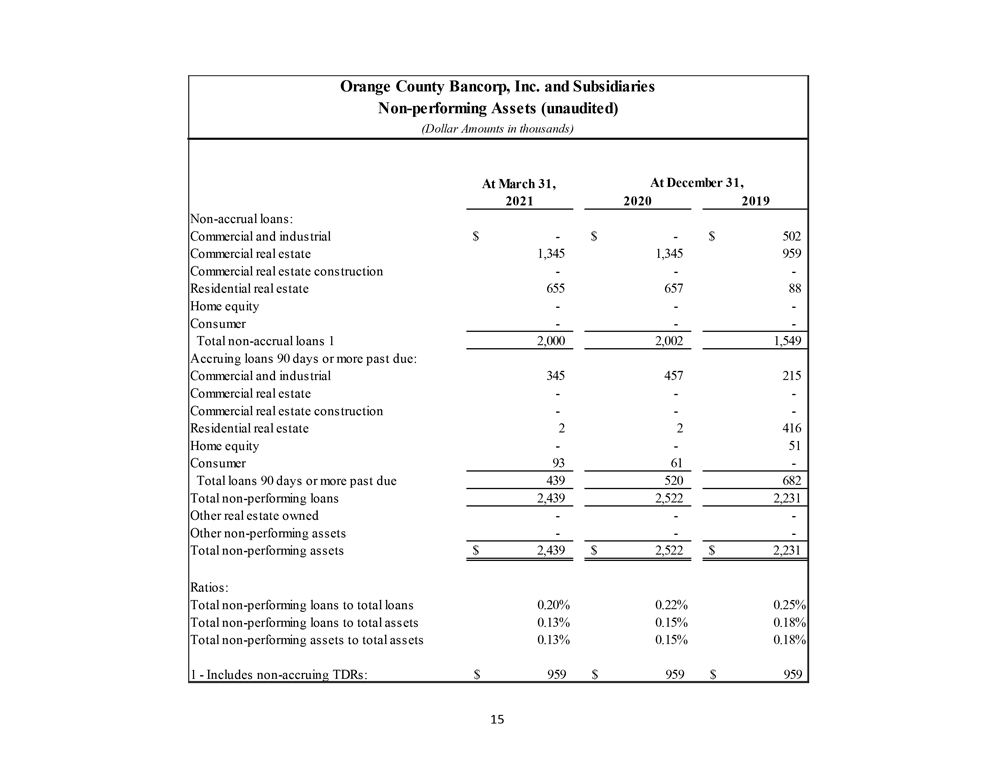

Loan Quality

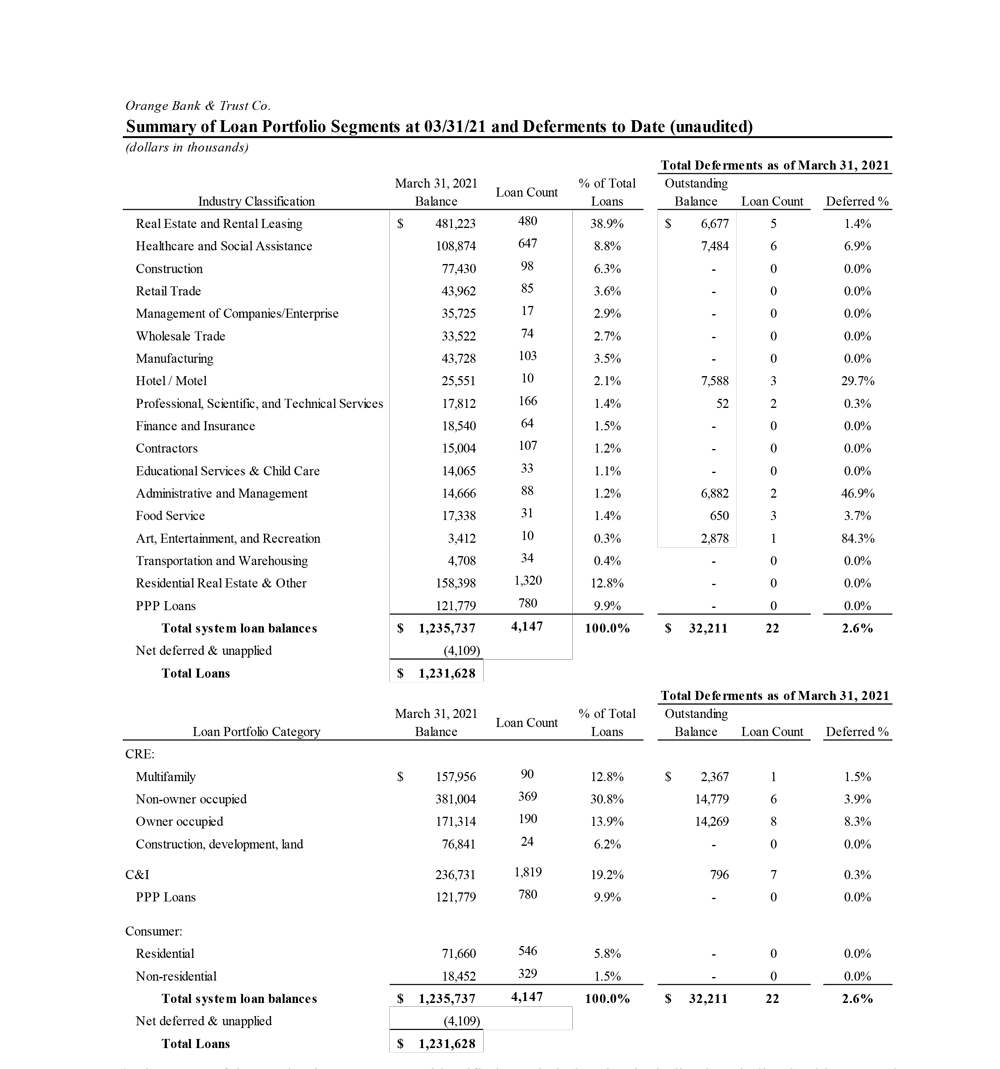

At March 31, 2021, the Bank had total non-accrual loans of $2.0 million, which included $959.0 thousand of Troubled Debt Restructured Loans (“TDRs”). This total was unchanged from year end 2020. Accruing loans delinquent greater than 30 days were $1.9 million as of March 31, 2021, compared to $1.8 million at December 31, 2020. The following table shows the current status of loans deferred as a result of the COVID-19 pandemic.

At the outset of the pandemic, management identified certain industries, including hospitality, healthcare, and retail, it viewed as most susceptible to stress from a prolonged slowdown in the economy. Notwithstanding perceived industry risks, portfolio concentration and exposure across these segments is modest. Notably, Lodging and Food Services, which broadly reflect our exposure to hotels, food and beverage, constitute $42.9 million, or 3.5%, of our loan portfolio. At quarter end, these categories accounted for 19.3% of total loans on payment deferral.

Management continues to evaluate performance trends across industry groups to assess underlying business and liquidity risks due to the economic impacts of COVID-19. While the Bank has continued to provide relief from debt service through forbearance agreements, its focus has shifted toward the resumption of loan payments, as management believes clients in need of deferral have largely been accommodated at this time. Most borrowers requesting deferral early in the cycle resumed scheduled repayment of their loan obligations at the end of their initial 90-day deferral period. Deferred loans at March 31, 2021 were $32.2 million, or 2.6%, of our portfolio, compared with $310.4 million, or 29.5%, of our loan portfolio at June 30, 2020.

Forward Looking Statements

Certain statements contained herein are “forward looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward looking statements may be identified by reference to a future period or periods, or by the use of forward looking terminology, such as “may,” “will,” “believe,” “expect,” “estimate,” “anticipate,” “continue,” or similar terms or variations on those terms, or the negative of those terms. Forward looking statements are subject to numerous risks and uncertainties, including, but not limited to, those related to the real estate and economic environment, particularly in the market areas in which the Company operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, changes in government regulations affecting financial institutions, including regulatory fees and capital requirements, changes in prevailing interest rates, credit risk management, asset-liability management, the financial and securities markets and the availability of and costs associated with sources of liquidity. Further, given its ongoing and dynamic nature, it is difficult to predict what the continuing effects of the COVID-19 pandemic will have on our business and results of operations. The pandemic and related local and national economic disruption may, among other effects, continue to result in a material adverse change for the demand for our products and services; increased levels of loan delinquencies, problem assets and foreclosures; branch disruptions, unavailability of personnel and increased cybersecurity risks as employees work remotely.

The Company wishes to caution readers not to place undue reliance on any such forward looking statements, which speak only as of the date made. The Company wishes to advise readers that the factors listed above could affect the Company’s financial performance and could cause the Company’s actual results for future periods to differ materially from any opinions or statements expressed with respect to future periods in any current statements. The Company does not undertake and specifically declines any obligation to publicly release the results of any revisions that may be made to any forward looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

About Orange County Bancorp, Inc.

Orange County Bancorp, Inc. is the parent company of Orange Bank & Trust Company and Hudson Valley Investment Advisors, Inc. Orange Bank & Trust Company is an independent bank that began with the vision of 14 founders over 125 years ago. It has grown through conservative banking practices, ongoing innovation, and an unwavering commitment to its community and business clientele to over $1.9 billion in Total Assets. In recent years, Orange Bank & Trust Company has added branches in Rockland and Westchester Counties. Hudson Valley Investment Advisors, Inc. is a Registered Investment Advisor in Goshen, NY. It was founded in 1996 and acquired by the Company in 2012. For additional information, visit orangebanktrust.com or hviaonline.com

For further information:

Robert L. Peacock

EVP Chief Financial Officer

rpeacock@orangebanktrust.com

Phone: (845) 341-5005